The Fintech ecosystem has been witnessing exponential growth with the onset of digital wallet and payment methods. With technology and innovation becoming more mainstream in the finance sector, it has opened doors for limitless opportunities for enhanced customer experience. But with opportunities comes some undeniable challenges and fintech security concerns are undoubtedly one of the most important concerns plaguing the industry today.

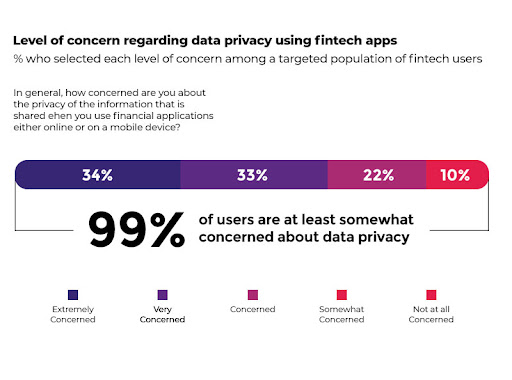

Financial institutions have suffered some major monetary losses owing to the increased cyber attacks. With full digitization of financial services underway, cyberattacks are increasing at an alarming rate. Financial institutions (22.5%) were the most common targets of phishing attacks in Q4 2020. What’s worse, financial services firms sometimes don’t even take notice of the data breach until it’s too late.

As financial institutions grapple with all kinds of cyber attacks, this article sheds light on the important cybersecurity concerns to be addressed when developing a Fintech application, regulations and policies prevalent in the industry and the emerging Fintech trends. Let’s delve deeper to explore each of these.

Fintech Security Concerns

A vast majority of financial institutions are heavily dependent on applications to facilitate transactions for end users. Developers of applications need to be mindful of the risks and challenges to be able to mitigate them effectively with appropriate security measures in place. Listed below are the top fintech security concerns that can hurt your business if left unchecked.

1. Data Security

Identity theft and data breaches is a top concern for the Fintech industry. Fintech companies use one-time passwords and other authentication methods to secure the payment system. However, hackers still manage to penetrate these systems to steal personal and financial information. In August 2021, Pine Labs, a B2B financial institution was reported to have been under cyberattack. The names and email addresses of the firm’s employees as well as confidential documents of the firm were allegedly exposed by a hacker group named Black Ransomware. Financial firms have always been under the risk of data breaches as cyberattacks are getting more sophisticated day by day and achieving complete security in the digital environment is quite an ordeal.

Source: The Clearing House

2. Cloud Computing Security Concerns

Gone are the days when data was stored in local data centres or personal computers. Cloud computing is now the backbone for online delivery of financial services. As cloud infrastructure gains more prominence, it’s important to watch out for a few security risks lurking around. Cloud computing for sure offers benefits of speed, accessibility and scalability. But with the vast amount of data flowing through the cloud, it’s easier for hackers to launch attacks. Financial firms need to ensure that the cloud services that they opt for are reliable. It won’t take long for a small breach to turn into an irrevocable loss. Misconfiguration of cloud resources is one of the leading causes of cloud computing security threats. A recent report suggests that around 49% of the finance firms were plagued by a cloud malware attack.

Source: TechTarget

3. Third-party Services

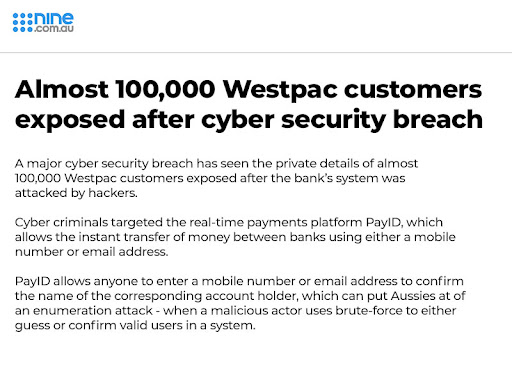

Third-party access is yet another security threat faced by banks and financial institutions. It’s common for financial firms to rely on third-party applications. But these third-party applications often serve as an entry point for hackers. They give hackers an opportunity to pose as legitimate users and gain unauthorized access, leading to compromised data security. When collaborating with third-party software, it is essential that financial institutions choose a trusted service. A good example of a third-party security breach would be the enumeration attack on Westpac Australian bank. The banking details of customers were exposed in mid-2019 when the hackers targeted PayID, a third-party platform that the bank partnered with to facilitate the easy transfer of money between banks.

Source: Finance.Nine

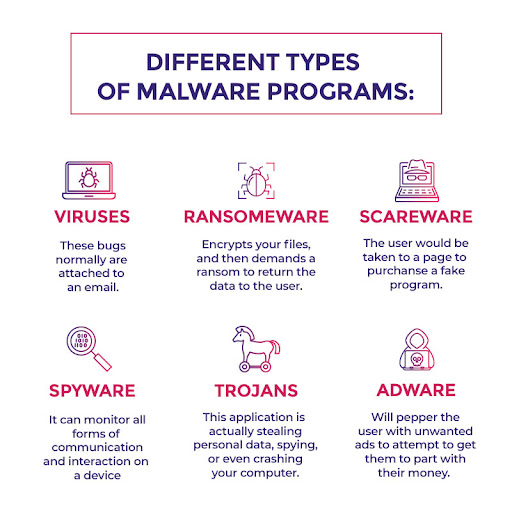

4. Malware Attacks

Malware attacks are the most common type of cyber threats plaguing the financial services industry. Users fall prey to malware attacks through third party software, emails or any other untrusted websites. Malware attacks can cause irreparable damage within a short period of time as it spreads faster. The Ministry of Electronics and Information Technology in India had alerted customers of major Indian banks earlier in 2021 about a malware being launched through an SMS link that claimed to be from the Income Tax department. Users were requested personal details upon clicking the link which was later misused by the hackers. The banking industry experienced a 1318% Y-o-Y increase in ransomware attacks during the first half of 2021, according to a recent report.

Source: Sectigo

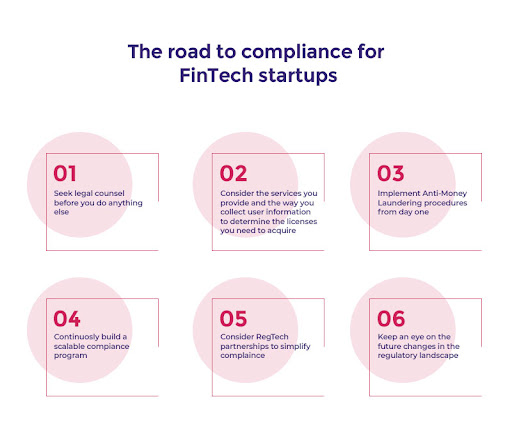

5. Compliance

Financial services firms are required to abide by certain standards and regulations to ensure security of sensitive information exchanged. Compliance is a serious challenge for fintech companies as it requires implementation of strict security measures so there remains no loophole that could be exploited by hackers. Plus, performance of applications and software must not be compromised while staying compliant. Some regulations are commonly applicable for all the finance institutions whereas some vary depending on the specific area that the firm is operating in such as lending/borrowing, insurance, financial advice etc. Failure to comply would mean hefty penalties for financial firms.

Source: Mindk

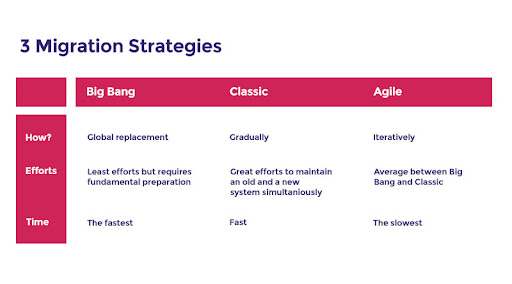

6. Existing Banking System Migration

Another important security concern is data getting exposed when migrating to newer systems. Fintech firms are replacing legacy systems with newer technologies at a rapid pace. While it is a move in the right direction, security is compromised during the transition. The more complex the migration, the higher the risk. Security lapses are bound to happen when a large amount of data is moved from here to there. The migratory period is a ripe opportunity for hackers to exploit the core banking system as security weakens. It is vital that fintech companies keep a weather eye on security issues during migration. The migration needs to be planned and executed with appropriate security controls.

Source: Diceus

7. Scalability and Financial Challenges

All fintech companies, regardless of their size, will have to scale their operations in future in pursuit of better opportunities for growth. Scaling infrastructure without compromising security is an important issue facing the fintech industry today. As companies scramble to deliver superior experiences to customers, it is vital to invest in technology and infrastructure that can keep up with modern day demands. At the same time, the fintech landscape is evolving constantly with new technologies, rules and regulations being introduced from time to time. As you scale infrastructure, it’s also important to give due attention to security measures. Staying compliant is important every step of the way and this requires significant financial investments. Frequent adapting to new technologies may prove expensive for firms but neglecting cybersecurity to save a few bucks can only result in long-term disastrous losses.

Fintech Regulations and Policies

Firms operating in the fintech industry are required to abide by certain rules and regulations. Firms in different countries may have to take the laws and regulations established by the respective authorities in that geographical area into account. However, listed below are some of the most important regulations governing the fintech industry today.

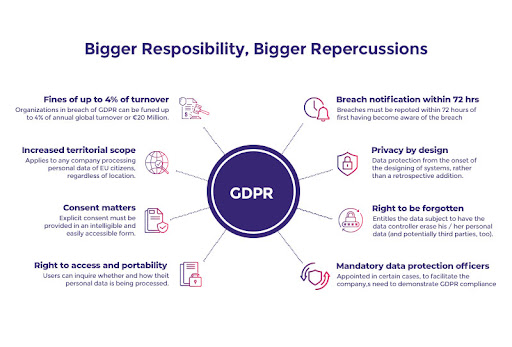

1. GDPR

GDPR stands for General Data Protection Regulation. It is a legal framework that governs the processing of personal information of European Union’s (EU) residents. This means any company that deals with personal data of European Union’s residents, irrespective of whether the company is located in Europe or not, needs to comply with GDPR. This rule came into full effect in May 2018.

Source: Emotiv

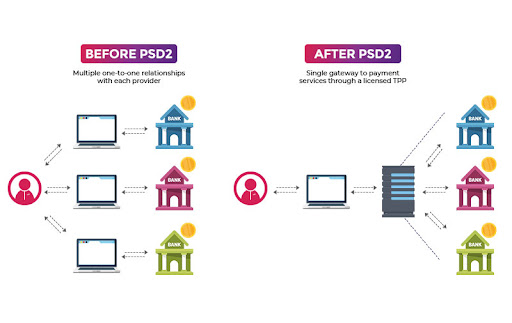

2. PSD2

The Payment Services Directive is a regulation that governs electronic payment services in the EU. This regulation mandates consent from account holders before their information is shared with third-party service providers. PSD2 improves security by guaranteeing strong customer authentication during online payments.

Source: Unnax

3. eIDAS

eIDAS is electronic Identification, Authentication and trust Services. eIDAS provides a common legal framework that makes cross-border electronic payments more secure. eIDAS facilitates secure online transactions between businesses, citizens, and public authorities. Any business dealing in electronic transactions is required to comply with eIDAS regulations.

4. FCA

FCA stands for Financial Conduct Authority. It is a regulatory body in the United Kingdom that has the consumer protection and protection of financial markets as its best interests. All fintech service firms are required to register with the FCA. FCA aims to promote healthy competition between financial service firms so consumers’ interests are protected.

Source: Kroll

5. GPG13

The Good Practice Guide 13 is a part of the UK Cabinet Office’s security policy framework. The GPG13 is a guide that must be complied to as a best practice. It deals with maintaining the integrity of internal systems with the help of network monitoring, events log management and intrusion detection systems.

6. APPI

APPI stands for Act on the Protection of Personal Information. APPI applies to businesses dealing with personal data of people in Japan. Businesses located outside Japan also need to comply with APPI if they ever deal with personal data of individuals in Japan.

7. PIPA

The Personal Information Protection Act is concerned with private data protection by private and government organisations in South Korea. Non-compliance with PIPA can lead to hefty fines being imposed on organisations as well as imprisonment. Evidently, it is one of the strictest data privacy laws in the world.

8. PCI DSS

Known as the Payment Card Industry Data Security Standard, this is applicable for entities dealing with credit card information. PCI DSS has specified four levels that service providers need to follow depending on the volume of transactions processed during the year. PCI DSS compliance protects fintech service providers from malicious online actors.

9. ISO/IEC 27001

ISO/IEC 27001 is a set of standards regulating protection of digital information. It outlines the requirements for maintaining a secure information management system. Compliance with ISO/IEC 2700l indicates that risks have been adequately managed by the organizations.

6 Major Security Trends Shaping The Fintech Industry

With an exponential rise in the number of cyber attacks on fintech firms and the subsequent financial losses, firms have tightened their security measures in an attempt to resist online attacks. Listed below are a few critical fintech trends shaping the security landscape in the coming years.

1. Artificial intelligence to detect frauds

Artificial intelligence(AI) has the potential to detect risks and has been relied upon by Fintech firms to strengthen security. With the advent of new technologies, fintech firms have a better opportunity to take a proactive approach towards cyber security. AI and ML systems can predict risks with effective analysis of customer and business data. It can scan through massive amounts of data to catch vulnerabilities and alert enterprises before the situation blows out of proportion.

2. SASE to consolidate security stack

SASE stands for Secure Access Service Edge. SASE solutions provide for comprehensive security within the system. SASE is based on a cloud-based infrastructure which helps consolidate security stack for fintech firms. It is a huge cost saver and eliminates the need to manage multiple security products. SASE ensures security for organizations regardless of where their users are located. SASE is critical for fintech firms as it can effectively prevent abuse of sensitive data.

3. Advent of advanced blockchain systems

Blockchain is disrupting the finance sector worldwide with its immense capabilities to reduce fraud. Blockchain is based on a decentralized network which ensures data integrity and transparency with its cryptographic algorithms. Transactions happening over blockchain are faster and more efficient. Individual blocks of data containing critical information are linked together which is difficult to decrypt, making it a more secure, reliable solution for fintech firms.

4. Increased reliance on Regulatory technologies

Regulatory technologies (Regtech) help address regulatory challenges in the financial sector. The list of regulatory obligations and compliances are growing with each passing year and RegTech is an answer to fill the gap and simplify monitoring of data and the process of compliance in general. RegTech with its big data analytics capabilities can help monitor and report in real time making compliance much easier.

5. Multi-cloud solutions for better security

Fintech firms are overhauling their data storage infrastructure with multi-cloud storage solutions. Multi-cloud data storage solutions facilitate efficient management of vast troves of data. A single public cloud system is not the best solution for fintech firms where security and compliance is of utmost importance. Multi-cloud data storage paves way for better transparency and yields cost-saving benefits in the long run.

6. Cutting-edge technology takes security to the next level

The fintech industry is leveraging new technologies to resist hacker attacks. AI, ML and blockchain technologies are utilized to strengthen security and reduce vulnerabilities and loopholes in the systems. Though hackers are launching more advanced and sophisticated attacks, fintech firms have new technologies at their disposal to protect data and prevent brute-force entry. Threat detection and zero-day attacks can be prevented today with security solutions evolving at a rapid pace. Moving forward, fintech firms are expected to invest in smarter security solutions to handle the huge influx of data without compromising on data integrity.

Final Thoughts

While the ‘first-to-market’ urge of firms may be blamed for some of the security lapses, it is no secret that the nature of cyber attacks have also become more sophisticated than before.

Fintech firms need to be constantly vigilant of the cybersecurity risks and build plans and processes around secure development of applications and systems. Security isn’t something to be taken into consideration after every other thing has been taken care of. It needs to be the topmost priority right from the moment an idea of developing an application or delivering services online has been conceived.

The cost of a security lapse extends beyond financial consequences as you put your customers’ confidential data and your own reputation at stake. Identify the risks, design security solutions, ensure compliance with applicable regulations and be prepared for any unforeseen security risks so as to minimize losses in the event of a breach. The major cyber security trends discussed above will sow the seeds for a safer fintech ecosystem in the near future.

AppSealing is a security solutions provider with rich experience and expertise in catering to businesses across industries. From gaming to Fintech, our solutions ensure robust security and scalable protection for Android, iOS and hybrid mobile apps without compromising app performance. Make data-based decisions in real time with threat analytics and prevent data theft while ensuring compliance with standards and regulations. Contact our team today for hassle-free implementation of top-notch security solutions!